Historical snapshot: The last time someone named Clinton stood on the verge of winning the White House, the annual total of projected U.S. construction starts was under $270 billion. And 25 Octobers ago, the young F.W. Dodge economist who took the stage for the first time before 500 building products executives to deliver that forecast was Robert A. Murray.

The more things change…

Last week, before a conference roomful of industry executives in National Harbor MD, Murray, now SVP and chief economist for Dodge Data & Analytics, climbed to the podium yet again to give the franchise’s 78th annual construction industry forecast. And his latest predictions, based on analysis of Dodge’s extensive “living library” of national project leads, call for an increase in U.S. construction starts of 5% in 2017, to a total value of $713 billion in new contracts. This follows four years of double-digit annual growth, which abruptly slowed this year to just an estimated 1% bump.

“The construction industry has now entered a more mature phase of its expansion, one that is characterized by slower rates of growth than what took place during the 2012-2015 period, but still growth,” said Murray, speaking last week at the #DodgeOutlook2017 conference. Following keynotes by Autodesk’s upbeat thought leader Stacy Scopano, and former hedge fund manager Steve Eisman — the prescient finance expert portrayed by actor Steve Carell in the film The Big Short — Murray was careful to ground his predictions in solid data.

“The construction industry has now entered

a more mature phase of its expansion”

Of course, given the nature of economic forecasting — which more than a few have likened to predicting the weather — everyone knows that even the best numbers-crunching is just an educated guess. So, with that in mind, and realizing that many in our industry still base at least some of their own budgeting and hiring decisions on such predictions, it is worth reviewing what Dodge Data sees on the near horizon.

“Total construction starts during the first half of this year lagged behind what was reported in 2015, raising some concern that the current construction expansion may have run its course,” noted Murray. “However, the early 2016 shortfall reflected the comparison to unusually elevated activity during the first half of 2015, lifted by 13 very large projects, valued each at $1 billion or more, such as a $9-billion liquefied natural gas export terminal in Texas and a $2.5-billion office tower in New York City. As 2016 has proceeded, the year-to-date shortfall has grown smaller, easing concern that the construction industry may be in the early stage of cyclical decline.”

Added Murray: “On balance, there are a number of positive factors which suggest the construction expansion has room to proceed. The U.S. economy in 2017 is anticipated to see moderate job growth, market fundamentals for commercial real estate should remain generally healthy, and more funding support is coming from state and local bond measures. Although the global economy in 2017 will remain sluggish, energy prices appear to have stabilized, interest rate hikes will be gradual and few, and a new U.S. President will have been elected.”

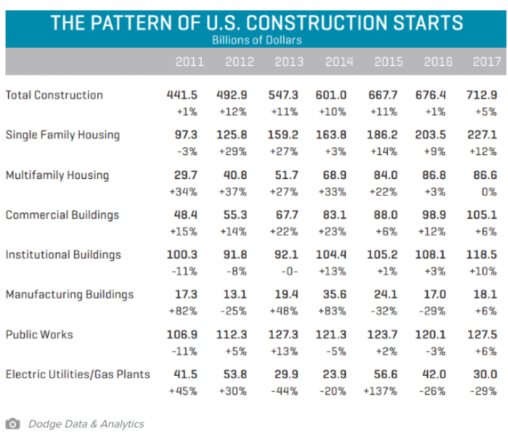

For 2017, supporting the predicted rise of 5% in the overall market, Dodge sees gains of 8% for both residential building and nonresidential building, while non-building work “slides a further 3%.”

Here’s how Dodge sees the pattern of U.S. construction starts playing out by sector:

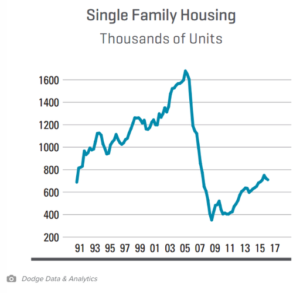

- Single-family housing will rise 12% in dollars, corresponding to a 9% increase in units to 795,000 (Dodge basis). Access to home mortgage loans is improving, and some of the caution exercised by potential homebuyers will ease with continued employment growth and low mortgage rates. Older members of the Millennial generation are now moving into the 30- to 35-year-old age bracket, which should begin to boost demand for single-family housing;

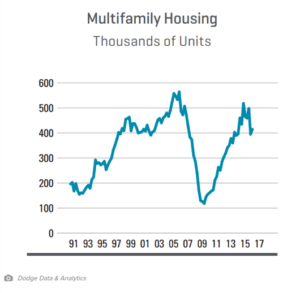

- Multifamily housing will be flat in dollars and down 2% in units to 435,000 (Dodge basis). This project type now appears to have peaked in 2015, lifted in particular by an exceptional amount of activity in the NYC metropolitan area, which is now settling back. Continued growth for multifamily housing in other metropolitan areas, along with still generally healthy market fundamentals, will enable the retreat at the national level to stay gradual;

- Commercial building will increase 6% on top of the 12% gain estimated for 2016. Office construction is showing improvement from very low levels, lifted by the start of several signature office towers and broad development efforts in downtown markets. Store construction should show some improvement from a very subdued 2016, and warehouses will register further growth. Hotel construction, while still healthy, will begin to retreat after a strong 2016;

- Institutional building will advance 10%, resuming its expansion after pausing in 2015 and 2016. The educational facilities category is seeing an increasing amount of K-12 school construction, supported by the passage of recent school construction bond measures. More growth is expected for the amusement category (convention centers, sports arenas, casinos) and transportation terminals;

- Manufacturing plant construction will increase 6%, beginning to recover after steep declines in 2015 and 2016 that reflected the pullback for large petrochemical plant starts;

- Public works construction will improve 6%, regaining upward momentum after slipping 3% in 2016. Highways and bridges will derive support from the new federal transportation bill, while environmental works should benefit from the expected passage of the Water Resources Development Act. Natural gas and oil pipeline projects are expected to stay close to the volume that’s been present in 2016;

- Electric utilities and gas plants will fall another 29% after the 26% decline in 2016. The lift that had been present in 2015 from new liquefied natural gas export terminals continues to dissipate. Power plant construction, which was supported in 2016 by the extension of investment tax credits, will ease back as new generating capacity comes on line.

To dive deeper into this data, before the inevitable updates and corrections, visit www.construction.com.

Discussion

Be the first to leave a comment.

You must be a member of the BuiltWorlds community to join the discussion.