![]()

How do active investors feel about the state of the built world venture capital market?

Introduction

Zacua Ventures published their 2024 Contech Investment Climate Survey report on February 7, 2024. The surveying of 114 VC and CVC construction tech (ConTech)-focused funds captured the market’s pulse and firsthand sentiments of 2024 ConTech investing. Key takeaways surround investment appetites, macro narratives, hot tech categories, and due diligence priorities.

Investment Appetite Trends

Overall, investment appetite for 2024 shows improvement compared to 2023. More investors anticipate either maintaining or increasing capital deployment this year compared to last (78% to 88% from 2023 to 2024, respectively).

In 2024, CVCs signal more conservative capital deployment strategies than VCs. 43% of CVCs anticipate increasing capital deployment, contrasting with 51% of VCs. Conversely, 12% of CVCs anticipate decreasing capital deployment, compared to only 6% of VCs. Additionally, 2% of CVCs intend to abstain from investing.

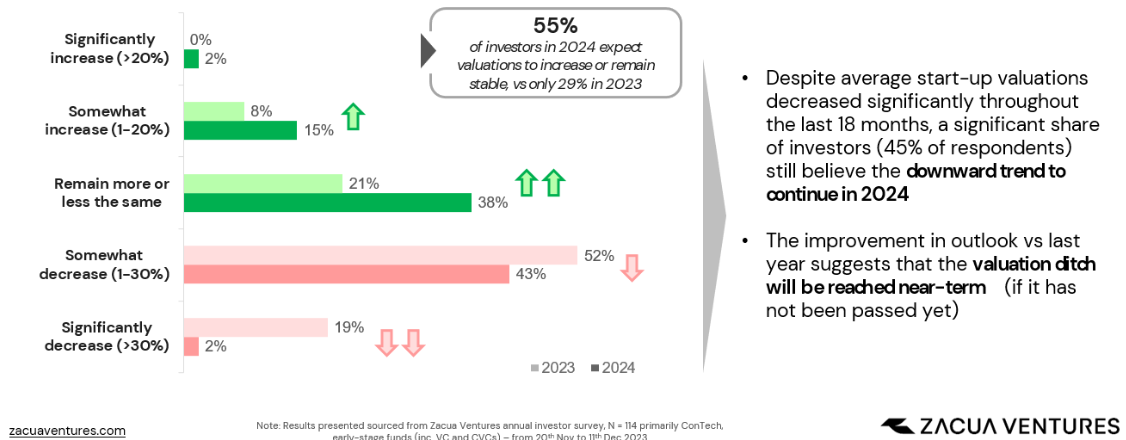

Macro Externalities & Investor Concerns

Three hesitations prevail from the current macroeconomic landscape: market uncertainty, valuation correction, and funds availability. Investors’ concern of market uncertainty and valuation correction have both been noticeably assuaged this year. Market uncertainty as a main fear for investing decreased from 61% in 2023 to 40% in 2024; valuation correction decreased from 38% to 32%, over the same period.

Improving valuation sentiments suggest they are at or near the bottom.

Source: 2024 Contech Investment Climate Survey, Zacua Ventures

However, not all investor fears are diminishing. The ability to fundraise is a rising concern amongst investors following the most difficult fundraising year in recent history. Funds availability as a main concern increased to 31% in 2024 from 29% in 2023.

Investors still remain demure about valuations as rate cuts are pushed further into the year. A slight majority–55%--feel that valuations will increase or remain stable this year. Although this is not an overwhelming majority, it marks a significant improvement from the 29% of investors who felt that way in 2023.

Hot Investment Categories

The Sustainability and AI investment craze persists. In 2024, sustainability as a preferred investment category has declined by 5% to 58%, compared to 63% in 2023. However, it is still the most preferred tech category by investors.

Half the survey respondents would like to increase investments in AI in 2024. To underscore the AI boom of 2023, AI was not even a category surveyed last year.

Zacua’s survey asked respondents to provide their top three priorities in the due diligence process.

Surprisingly, management team expertise as a top three investment criteria decreased from 88% to 77% from 2023 to 2024. This was identified in the 2023 Annual Venture Report as the primary component of the flight to quality investment mentality.

Concurring with the 2023 Annual Venture Report, Zacua’s survey revealed that product traction importance is increasing in 2024. The frequency of this as a top three factor increased from 58% in 2023 to 63% in 2024.

Unsurprisingly, investors are placing less importance on cash burn rates in 2024. Macro pressures, such as inflation and high cost of capital, have left burn rates uncharacteristically high across the board leading investors to accept this as par for the course.

Conclusion

Overall, ConTech investors feel better about the VC market in 2024 than 2023, aside from hesitations on the availability of funds and some reverberating macro pain points.

Zacua’s survey showed an increase in ConTech deal count from 2022 to 2023, while deal valuations declined over the same period. Zacua chalked this up to less later-stage deals. BuiltWorlds’ 2023 Annual Venture Report tracked slightly different deal trends in the space.

Furthermore, residential construction project backlogs continued to get pushed causing companies to undertake fewer new projects during the year. Lower residential project adoption is expected to lead to startups targeting civil, infrastructure, and industrial applications in 2024.

Built world venture investing continues to outperform the overall VC market for another year as the lagging industry bolsters tech adoption.

Curious about how BuiltWorlds’ State of the Built World Annual Venture Report aligns or differs from Zacua’s ConTech report?

Discussion

Be the first to leave a comment.

You must be a member of the BuiltWorlds community to join the discussion.