As 2023 Q4 earnings announcements wrap up and Q1 2024 earnings are entering the crosshairs, the BuiltWorlds Venture and Investments team examined trends of public AECO companies’ financials through FYE 2023. For this earnings roundup, we analyzed Procore (NYSE: PCOR), Autodesk (NASDAQ: ADSK), Trimble (NASDAQ: TRMB), CRH Plc (NYSE: CRH), Deere & Company (NYSE: DE), and Caterpillar (NYSE: CAT).

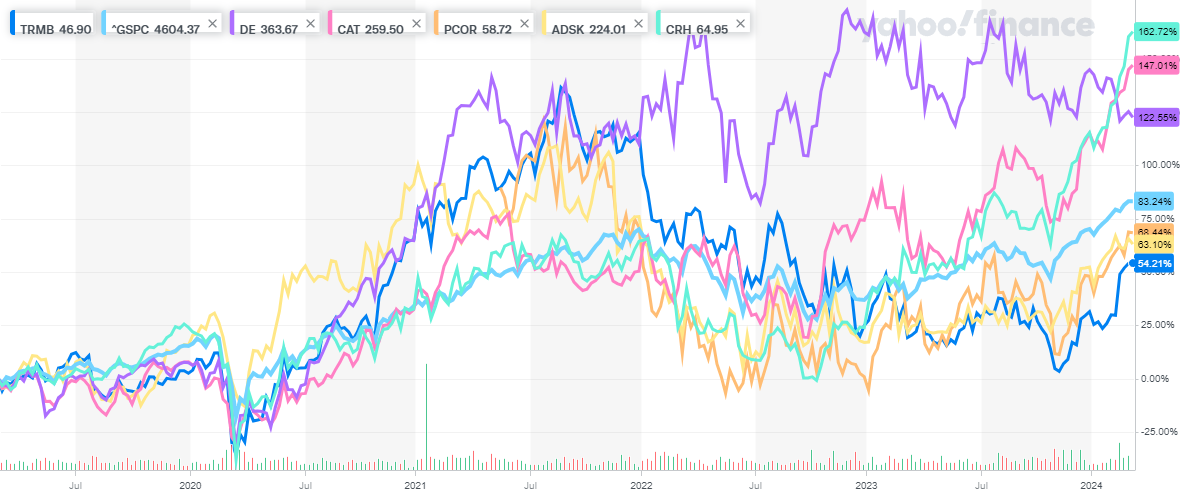

The chart above depicts the performance of the five stocks compared to the S&P 500 index (labeled as “^GSPC” in the legend at the top left) over the last five years in terms of percentage return. A clear delineation emerged: Caterpillar and Deere have consistently outperformed the S&P - or the “market” - with CRH joining the club as of 2022; meanwhile, Autodesk, Procore, and Trimble have underperformed compared to the market.

The market has pinned blue collar (Deere, Caterpillar, and CRH) against SaaS (Procore, Autodesk, and Trimble) with blue collar emerging as the heavy favorite. The question is: why?

Margins

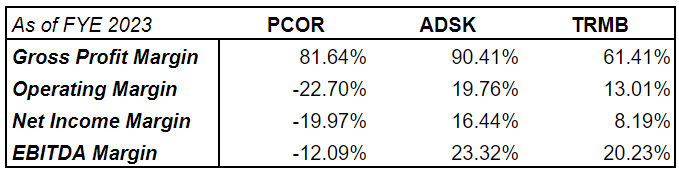

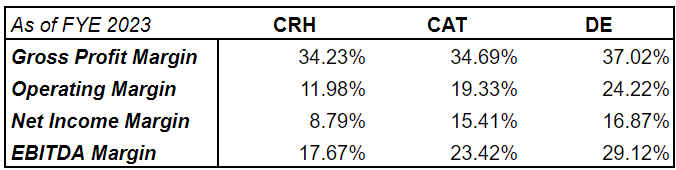

Construction SaaS companies are not delivering SaaS margins.

Gross profit, operating income, net income, and EBITDA as a percentage of revenue, or margins, are how investors determine a company's efficiency at mitigating expenses and generating revenue. With much of these SaaS companies’ expenses tied up in the “sales, general, and administrative” line item under operating expenses, a precipitous narrowing of the margins is observable between each company’s gross profit and operating income.

SaaS companies are commonly expected to have high margins due to their recurring revenue model and low direct costs. The construction SaaS companies have failed to maintain their gross profit margin advantage by overloading their income statement with high overhead costs, especially in the sales and marketing departments.

Although they aren’t delivering 90% gross margins, the blue collars are able to retain consistent margins all the way down the income statement. The honorable range of operating expenses from 8.8% to 16.9% exhibited in this sample shows adequate capital efficiency from an unassuming sector of the public markets.

Cash Flow

EBITDA (earnings before interest, taxes, depreciation, and amortization) is commonly viewed as a proxy for a company’s true cash flow. The SaaS companies' choppy cash flow generation amidst the blue collars' consistency also provides a rationale for the market sentiments.

Procore has made material improvements, but is still a far cry from profitable. As of FYE 2023, Procore’s EBITDA increased to -$114.8M from -$221.3M the prior year, a 48.1% increase. Procore's net loss improved from $286.5M to $188.4M, a 33.9% improvement. It took Amazon seven years to turn profitable as a SaaS business; Procore, in its 22nd year, is now making substantial strides in the right direction.

Trimble experienced its third straight year of declining EBITDA. Trimble’s EBITDA declined from $812M in 2022 to $768.6M in 2023, a 5.3% decline from the year prior.

Autodesk, on the other hand grew EBITDA from $778M in 2022 to $1.2B in 2023, a 50% increase. Despite its strong EBITDA growth over the last three years, Autodesk's net income has been choppy during the same time period. In 2022, net income fell from $1.2B to $497M (a 58.9% decrease), then increased to $823M (a 65.6% improvement) in 2023.

While the market is signaling difficulty in understanding how to treat these mercurial construction SaaS companies, it does realize the value of the blue collars.

Deere expanded EBITDA by 44.6% in 2022 and then remained constant at $17.5B in 2023. Caterpillar grew its EBITDA by 37.6% to $15.7B in 2023, and CRH by 17.7% to $6.2B. Constant, predictable cash flows and efficient capital management continues to trump the nascent, yet promising, tech sector in the built world.

Discussion

Be the first to leave a comment.

You must be a member of the BuiltWorlds community to join the discussion.